Realistic Finances 🏁

I’m sure we’ve all heard the stories on Dave Ramsey’s show.

We paid off $150,000 of debt in 7 months making $50,000 a year. Or you’ve been following the FIRE (Financial Independence Retire Early) movement and heard stories of people retiring in their 30’s.

When we hear these stories we are filled with hope and optimism. Then we go home, crunch the numbers and it turns out that it’s going to take us a decade or more to pay off our debt and we can’t even consider early retirement, let alone retiring in our thirties. This feels discouraging doesn’t it? We look at other people and their stories, compare ourselves to them, and then wonder where it all went wrong.

Well after meeting with thousands and thousands of clients over my career, I’m here to tell you that these seemingly impossible stories are the exception to the rule. They’re more rare than you think and shouldn’t discourage you from setting up a financial plan. The only people I’ve seen fail at their finances are the ones without a plan. Those that have a plan, and are trying to stick to it, turn out fine.

So where do we start? First of all, you need to see if you’re still taking on debt. Stop spending money you don’t have to. You’re going to have to look at your expenses by printing out that last few months of bank and credit card statements, then categorize your spending. If the amount spent is greater than what you earned, YOU HAVE TO CUT BACK ON SPENDING. Lower your car insurance, stop eating out as much, stop buying clothes, cut your gym membership, ditch the satellite tv, whatever it takes to stop sinking further into debt. This can be a hard step to take, but do not give up.

Once you’re spending LESS that you’re bringing in, you start to look at paying down debt. Start with a small amount of your monthly income and start throwing it at the debt.

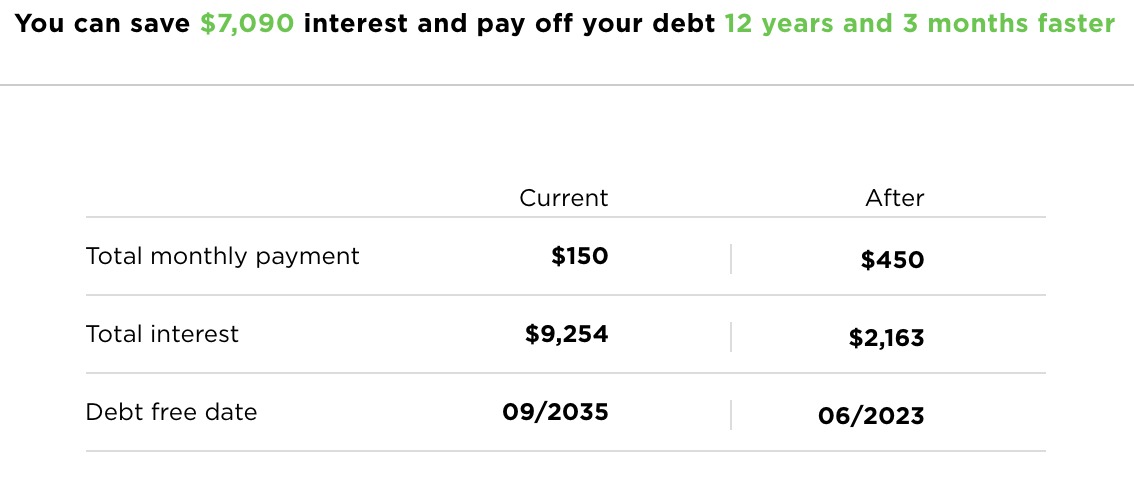

Let’s use $300 as an example. If you have take-home pay of $3,000/month, this is 10% of your net income.

If you have $20,000 of new debt, it has a 5% rate, you’re making a $150 payment AND you’re putting 10% of your take-home pay towards your debt, it will be paid off in June of 2023. Boring. Seems like forever. But if you don’t start, it may take decades to pay off.

What if you want to pay it off faster? Well put more of your take-home pay towards the debt. Snowball or Avalanche the debt payments (more on that here). Maybe, pick up an extra shift. Start a side hustle. The key is that you MUST start somewhere. Once you set a baseline number, DO NOT deviate from that. Your future self will thank you.

HINT: Do not compare yourself to others. Let them do them and you do you. Who cares what they’re doing? Be happy with your accomplishments. Let me tell you, if you start doing this, you’re already exceptional. Don’t give up.

I listen to this almost everyday for motivation (NSFW).

If you’d like to work with a Financial Planner to start getting a handle on your debt, contact us here.